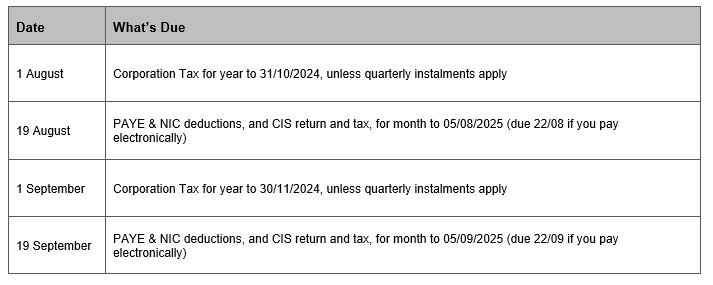

Covid Business Interruption Insurance settlement

We wanted to share great news from one of our clients who has just received a Covid Business Interruption Insurance settlement for over £80k!

Her claim had been rejected a number of times over the years, however recent Court cases and rulings have now meant that you could also be eligible for a payout.

The firm that secured the settlement is now offering to review on a ‘no win no fee’ basis any of our Clients policies to see if they also have a claim – please read the below to find out which Insurers this applies to and if you think that you may be eligible and would like your policy and cover checked, please contact your client manager.

Was Your Covid Business Interruption Claim Rejected?

Q1 (Insurer Group 1) – In 2020, if your Insurer was Eaton Gate, Morgan Richardson, Argo, AIG, Arista, Salon Gold or Beazley or you know anyone who may have been in the Hospitality Industry, or Hair / Salon / Barbers, it would definitely be worth having your Policy and Cover re-checked – please get in touch immediately as these Claims can be progressed without Court Action

and

Q2 (Insurer Group 2) – If your Insurer in 2020 was Royal Sun Alliance, AXA, Liberty Mutual, Marker Study, Ageas and Accelerant, then you may be able to join the Group Action claim

For Insurer Group 2, you may qualify if:

- Someone on your premises exhibited Covid symptoms between 5–20 March 2020..

- You held a Business Interruption insurance policy with Royal Sun Alliance, AXA, Liberty Mutual, Marker Study, Ageas or Accelerant.

- You were mandated to close by the government’s ruling.

A group action is currently being prepared against these six major insurers, to force them to pay the money they owe innocent businesses, however there is a very short window to join this group claim in order to meet the deadline.

What to do:

Solicitors are now preparing the case against these six insurers, and all claims will be handled on a no win, no fee basis. But the clock is ticking as the legal deadline to submit claim to court is November 2026, and time is needed to assess and prepare your case before then. Don’t delay or you risk missing out.

If your insurer turned you down, this may be your final opportunity to recover what you are owed.