Welcome to our December 2024 tax news!

Our monthly newsletter covers a range of tax related topics as well as celebrating what we’re doing as a company.

Topics covered this month includes:

- A new chapter of leadership for Gascoynes.

- Farmers campaigning for Agricultural property rethink.

- Check your state pension entitlement.

- Fundraising update for Parkinson’s UK.

- Christmas updates – including paying employees early before Christmas, Employee Christmas gifts and our Christmas closure dates.

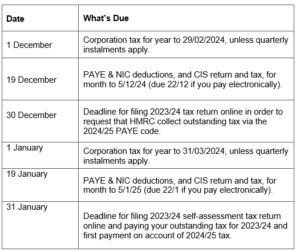

You’ll also find below useful dates for your diary this December and January.

Please contact us if you have any questions regarding any of the articles or if you would like further information on a topic we haven’t covered.

Have a great Christmas and best wishes for 2025!